monsitj

Dear Investor:

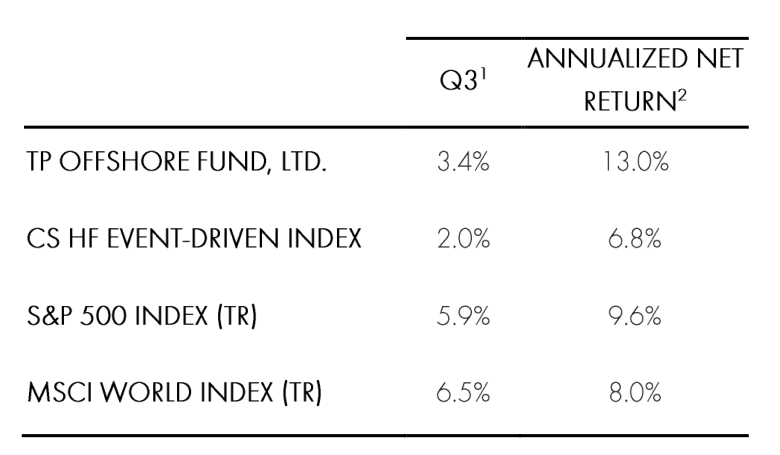

During the 3rd quarter, Third Point (OTCPK:TPNTF) returned 3.9% in the front runner Offshore Fund.

OTCPK:TPNTF) returned 3.9% in the front runner Offshore Fund.” contenteditable=” incorrect” loading=” careless”>

OTCPK:TPNTF) returned 3.9% in the front runner Offshore Fund.” contenteditable=” incorrect” loading=” careless”>

|

1 Through September 30, 2024. Please note there is a one-month lag in efficiency showed for the CS HF Event-Driven Index 2 Annualized Return from beginning (December 1996 for TP Offshore and estimated indices). PLEASE SEE THE BRAND-NEW COLLECTION RETURNS AT THE END OF THIS PAPER. |

The leading 5 champions for the quarter were a personal setting in R2 Semiconductor, Pacific Gas andElectric Co (PCG),Vistra Corp (VST), KB Home (KBH), andDanaher Corp (DHR)

The leading 5 losers for the quarter, omitting bushes, were Bath & &Body Works Inc (BBWI),Amazon comInc (AMZN),Advance Auto Parts Inc (AAP),Alphabet Inc(GOOG,GOOGL )and Microsoft Corp.(MSFT)

EVALUATION AND OVERVIEW 1

During the 3rd quarter,Third Point Offshore created gains of virtually 4%, bringing year -to-date go back to 13%, web of charges and expenditures. Global equity markets proceeded their solid efficiency, yet returns were driven by significantly even more market breadth than over the previous year and a fifty percent. The “Magnificent Seven” routed the wider market (albeit decently) for the very first time considering that Q4 2022. Rate delicate supplies and cyclicals dramatically exceeded as the marketplace moved its emphasis to the Fed’s long-awaited alleviating cycle. As we highlighted in our Second Quarter letter, our profile has a wide variety of financial investment motifs beyond huge cap technology. These sorts of financial investments in industrials, energies, products, and various other housing-sensitive supplies led the profile for Q3.

For a lot of the virtually thirty years I have actually run Third Point, the marketplace has actually been necessarily climbing up a wall surface of concern. At times, the concern transforms to misery, most just recently initially of August, when the Nikkei (NKY:IND) inexplicably tanked approximately 20% in a couple of days and volatility in the United States took off to virtually 70 from 16, all while United States markets went down 6%. Many experts saw this as a caution that the marketplace had even more area to go down which, in the very best situation, supplies had actually ended up being “un-investable” via the political election. While we took our swellings for a couple of days, we remained dedicated to our placements, took the sight that the marketplace turning would certainly proceed, and enhanced our financial investments in event-driven and value-oriented supplies.

Considering political growths over the previous couple of weeks, our team believe that the possibility of a Republican triumph in the White House has actually enhanced, which would certainly have a favorable influence on particular fields and the marketplace generally. We think the suggested “America First” plan’s tolls will certainly boost residential production, framework costs, and rates of particular products and assets. We likewise think that a decrease in guideline normally and particularly in the lobbyist antitrust position of the Biden-Harris management will certainly release performance and a wave of company task. Accordingly, we have actually enhanced particular placements that might gain from such a situation by means of both supply and choice acquisitions and remain to change our profile far from business that will certainly not. Whatever the end result of the Presidential political election, we have actually very carefully researched the Senate races and think that the Republicans will certainly develop a bulk, restricting the financial drawback of a “Blue Sweep” which might in theory introduce squashing tax obligations, suppressing laws, and a headwind to development.

In the economic climate, we see no proof of economic crisis, slowing down rising cost of living, and an actual rates of interest that still requires ahead down. We think healthy and balanced customer costs and energetic degrees of specific investing must give a liquidity background to maintain market degrees. We believe this arrangement is a specifically great one for event-driven investing, especially considering that a lot of our rivals around have actually retired or carried on. The possibility for threat arbitrage deals and company task might introduce a golden era for the method. At this factor, our gross direct exposures are reduced, we have moderate webs, are well placed in our present profile, and can release fresh resources as chances occur.

Equity Updates

DSV (OTCPK:DSDVF)

During the Third Quarter, we launched a brand-new setting in the Danish products forwarder DSV. DSV has actually come a lengthy method from its beginnings as a Nordic road-hauler to end up being the globe’s 3rd biggest products forwarder, with a powerful performance history of combining the fragmented worldwide products forwarding market. We think the firm has an excellent society that is systems-driven and returns-focused. DSV has actually created a roughly 20% EPS CAGR over the previous ten years and is commonly identified as the best-in-class driver, with market- leading development and earnings margins.

DSV became the leading prospective buyer in the public auction of DB Schenker, a subsidiary of German state-owned Deutsche Bahn AG, and among its biggest rivals. DB Schenker is comparable in dimension to DSV yet just fifty percent as successful. We think the assimilation and harmony capture anticipated from this mix will certainly comply with a tried and tested playbook and drive incomes increase over of 30%. We have actually assessed DSV’s numerous purchases and observed that they comply with a pattern of promptly moving the target onto DSV’s IT system, choosing low-margin organization, and rightsizing the expense framework, leading to the target’s margins getting to DSV’s best-in- course margins within 2 years.

The DB Schenker purchase is occurring at an intriguing time. Following a duration of post-COVID incomes normalization and a chief executive officer adjustment, DSV’s supply was trading at an approximate 20% discount rate to both its lower-growth peers and its historic numerous. Following the bargain, DSV will certainly be the biggest gamer in a sector in which range brings substantial expense and network advantages. An instance of this blessed affordable positioning is that DSV was picked as the special logistics carrier for Saudi Arabia’s NEOM task. We think the joint endeavor in between DSV and Saudi Arabia will certainly give end-to-end supply chain monitoring, establish transportation and logistic properties, and expand the firm’s incomes power by around 15% by 2028.

We have actually hung around with Jens Lund, DSV’s long period of time COO/CFO that ended up being chief executive officer previously this year and have actually discovered him to be laser-focused on producing investor worth.Mr Lund made an engaging situation that increasing intricacy in worldwide supply chains will certainly profit DSV, as it monetizes its special network that ensures capability and on-time shipments. In the products forwarding market, straightforward tons, A-to-B transport is hardly successful. The genuine cash is made from value-added solutions such as custom-mades clearance, tons combination and treatment when troubles happen, a core proficiency of DSV. We think DSV can gain greater than 100 DKK per share in 2027 and see substantial benefit for among Europe’s ideal business.

Cinemark (CNK)

Earlier this year we took a risk in Cinemark, the 3rd biggest cinema chain in the united state We think Cinemark is positioned for underappreciated development over the following couple of years as the supply of theatrical launches recoils from pandemic- and strike-related headwinds. In enhancement, our team believe Cinemark will certainly obtain share from undercapitalized rivals.

There is no scarcity of doubters concerning the relocation cinema organization. In 2020 the overview for residential movie theaters looked grim: the fast increase of streaming, incorporated with habits adjustments from the pandemic, called into question whether individuals would certainly ever before most likely to movie theaters once again. Regal Cinemas applied for personal bankruptcy. AMC ended up being a meme supply.

Against this unpromising background, Cinemark has actually shown durable monetary efficiency. Consider that in 2023, counterintuitively, Cinemark reported greater cost-free capital than they performed in both years before the pandemic. Yet, Cinemark supply went into 2024 trading 70% listed below pre-pandemic degrees (a mid-single number numerous on routing 12-month cost-free capital), recommending market individuals was afraid cost-free capital would certainly go down precipitously and never ever recoup. We differ with this sight and think the multi-year overview for Cinemark has actually never ever been even more durable.

Despite the current success of movies such as “Inside Out 2”, 2024 market profits are anticipated to end up at roughly $8.5 billion, over 20% listed below pre-pandemic degrees. While numerous out there feature this to transforming customer choices, the information shows movie theaters are a supply-driven market (even more movies amount to even more foot web traffic), and our team believe the vital vehicle driver of weak ticket office profits has actually been a 20% decline in widescreen theatrical launches considering that 2019. Importantly, our team believe that this is driven by intermittent variables, specifically labor interruptions from the pandemic and consequently the strikes, instead of nonreligious variables. Over the previous 3 years, ventures right into special streaming and day-and-date launches have actually confirmed as well unlucrative, and the “event” element of a staged launch has actually confirmed important to safeguarding leading skill and producing franchise business IP that can drive future incomes. As an outcome, all 6 significant Hollywood workshops have actually dedicated to ramp quantity back up to pre-COVID degrees, and also pureplay banners like Amazon and Apple (AAPL) have actually started launching movies specifically in movie theaters. We anticipate supply to rebound following year and get to the pre-COVID degree by 2026, which we anticipate to drive a complete healing in ticket office profits as decently reduced per-film participation is balanced out by cost rises and development in giving in profits. In our sight, short-term headwinds from the 2023 Hollywood strikes were concealing this essential nonreligious change in movie supply, which offered us the chance to launch the financial investment at a dislocated appraisal.

Cinemark’s incomes outperformance versus its peers via the pandemic has actually not been a crash; while AMC and Regal have actually been shutting displays and underinvesting to maintain liquidity, Cinemark utilized what we view as a solid annual report and unrelenting concentrate on expense effectiveness to receive upkeep capex in their movie theaters regardless of the tested operating background. As an outcome, the firm has actually taken control of 100 bps of market share, a fad we view as lasting as peers remain to justify their impact regardless of a boosting market.

Given the substantial healing in ticket office, possibility for ongoing share gain and high operating utilize of business, we believe Cinemark can produce over $4 of FCF/share in 2026, which is meaningfully greater than pre-pandemic degrees and must expand in the adhering to years. The firm revealed it will certainly set out its long-lasting resources allowance method in very early 2025, consisting of a re-introduction of a returns, which must be helpful of an ongoing re-rating in the shares.

Credit Updates

Corporate Credit

Third Point’s company debt publication created a 3.5% gross return (3.4% web) throughout the quarter, adding 50 basis indicate efficiency. That places year-to-date efficiency at +8.3% gross (8.2% web), in accordance with the high return index. The summertime verified anything yet terrible for high return, with the marketplace returning 5.3% throughout the quarter, in accordance with the solid efficiency of the S&P 500. Spreads tightened up partially with a lot of the return driven by the decrease in rate of interest.

While some financial task has actually been revealing indicators of slowing down, the protective make-up of the present high return market with a high mix of better debt and brief period has allow the prices tailwind bewilder such worries. The least expensive high quality fields of the marketplace have actually executed best, sustained by both soft/no touchdown assumptions, in addition to 2 favorable occasions in the beleaguered telecommunications area. Telecom/ wire have actually been bad entertainers year to day as a result of overhang from the development of FWA (also known as “wireless cable”) and enhanced fiber structure, nevertheless the industry re-rated materially on 2 offers. First, Lumen Technologies (LUMN) revealed that its Level 3 (LVLT) subsidiary was doing a fiber framework construct to sustain AI development. Our hostility to nonreligious decrease (a lot of LUMN is melting copper framework) maintained us out of the circumstance yet the AI fairy dirt caused an enormous rerating of LUMN financial debt and equity. These greater safety rates consequently promoted a number of transfer to re-finance parts of the resources framework and expand the path.

Second, Verizon (VZ) revealed an offer to obtain Frontier Communications (FYBR), a purchase which the fund took advantage of through its financial investment in FYBR financial debt. This purchase, targeted at raising’s VZ fiber impact, has actually caused wide revaluation of fiber retail networks that we believe is proper. While we remain to anticipate to see FWA swiftly deteriorate non-upgraded wire and particularly copper’s share of the low-end broadband market, the VZ bargain emphasizes the worth of the greater end impact.

Much has actually been discussed “creditor on creditor violence”– responsibility monitoring offers where providers have the ability to decrease their expense of resources or expand liquidity paths by using a part of lenders an opportunity to go up the resources pile at the expenditure of their brethren. These are often much less than absolutely no amount offers for lenders and largely advantage monetary enrollers, and a a great deal wind up reorganizing anyhow after paying substantial charges to attorneys and consultants. As an outcome, we are seeing an increasing variety of financial institution “co-op agreements”, which offer to avoid enrollers from controling lenders. While we have actually normally been extremely cautious to place ourselves on the winning side of these altercations, we delight in to see the increase of these co-op contracts. Co- ops can make purchasing extremely worried circumstances a lot more eye-catching due to the fact that you can rely on that an elderly responsibility does not obtain leapfrogged by a jr responsibility. Additionally, it promises that these co-ops will certainly speed up the rate of restructurings, considering that enrollers will certainly have restricted choices to get time to stay clear of equity write-offs.

While the high return market has actually rallied, we have actually remained to discover chance in a couple of locations. We have actually purchased right into a number of credit scores that have actually experienced responsibility monitoring offers. These companies were enhancing, and recapitalization was thorough adequate to “fix” the annual report. We are likewise discovering worth in a number of loan-only frameworks that have actually delayed the rally in the high return market.

Structured Credit

The Structured Credit profile added 20 basis factors in the quarter, driven by Treasuries and debt spreads rallying. While the Treasury market has most likely overstated the size of possible Fed price cuts for this year, we capitalized on that market home window and exercised our phone call civil liberties on 8 reperforming home loan offers this quarter. We valued a brand-new home loan securitization in August with AAA’s prices within 5%, closer to financial investment quality returns we saw in 2019 and very early 2020. As insurance provider and exclusive credit scores funds proactively seek financial investment quality threat, we have actually had the ability to accessibility, in our sight, eye-catching expense of funds throughout organized debt finances. Given the decrease in brand-new home loan sources and freshly released mortgage-backed protections, we have actually seen a renovation in the technological background for existing protections and finances. We think this vibrant offers us a benefit as we remain to market and maximize our existing home loan profile.

On the abdominal muscle front, returns have actually remained to press throughout all possession courses. Spreads have actually continued to be greatly the same on our rental vehicle abdominal muscle profile, which we purchased previously this year at dual number returns. This has actually been a favorable profession for the profile as we understand substantial bring monthly. We have actually been monetizing our abdominal muscle placements right into this debt spread tightening up and are investing even more time on CLOs and CMBS as debt occasions begin to play out.

As we encounter geopolitical unpredictability and an unpredictable rates of interest atmosphere, we prepare for intriguing financial investment chances in the Fourth Quarter as financiers seek to safeguard a strong 2024 efficiency.

Private Position Update: R2 Semiconductor

In March, we revealed that we were sustaining R2 Semiconductor, a personal firm in our Third Point endeavors profile that we purchased over 15 years previously, as it looked for to apply its trademarked innovation versusIntel The innovation, established by R2’s Founder David Fisher, connects to incorporated voltage guideline, which plays an important part in lowering power usage by integrated circuits while keeping item integrity.

At completion of August, Intel revealed that its disagreement with R2 had actually been totally resolved in all territories. The terms are personal, yet we are pleased with the end result, which caused a considerable gain in the setting for the quarter.

Business Updates

Matthew Ressler signed up with Third Point’s exclusive debt group in Q3. Prior to signing up with Third Point,Mr Ressler invested 4 years at Apollo Global Management as a financier in the Private Equity Group, with an emphasis in the innovation, industrials and customer fields.Mr Ressler likewise formerly operated at Moelis & & Company as an Associate in the company’sInvestment Banking department after starting his job at JPMorganChase Mr. Ressler holds an MBA from Harvard Business School and a B.A from Dartmouth College.

Ted Smith-Windsor signed up with Third Point in Q3, concentrating on debt financial investment chances. Prior to signing up with Third Point,Mr Smith-Windsor operated at Silver Point Capital where he concentrated on financial investments in troubled debt and unique circumstances. He started his job at CPPIB where he concentrated on financial investments secretive equity and debt.Mr Smith-Windsor is a grad of the University of Toronto, where he made a B.Comm in Finance and Economics.

Maureen Hart signed up with Third Point in Q3 as Head ofConsultant Relations Prior to signing up with Third Point,Ms Hart was a Partner atAlbourne America Over her 12 years at Albourne, she supervised most of the company’s North American customers, handled an international 50-person group, and led the company’s cross-selling campaign.Ms Hart started her job in Investor Relations at FrontPoint Partners, covering equity long/short funds. She finished from the University of Connecticut with a B.A. in English.

Thomas Anglin signed up with Third Point in Q3 as Head of Marketing and Business Development for the Asia-Pacific area. Prior to signing up with Third Point,Mr Anglin was a Managing Director at Goldman Sachs in Hong Kong where he supervised protection of hedge fund supervisors in Asia and was in charge of Goldman Sachs’ Australian Prime Brokerage organization. Previously, he held elderly management placements at Goldman Sachs in New York, UBS Investment Bank in New York and Sydney, and was an equities and assets investor atOspraie Management Mr. Anglin began his job in equity by-products sales and trading at Macquarie Bank in Australia and transferred to New York with Macquarie in 2000. He obtained a B.Com from Monash University in Melbourne and is a CFA charterholder.

Sincerely,

Daniel S. Loeb CHIEF EXECUTIVE OFFICER

|

The info consisted of here is being offered to the financiers in Third Point Investors Limited (the “Company”), a feeder fund detailed on the London Stock Exchange that spends significantly every one of its properties in Third Point Offshore Fund, Ltd (“Third Point Offshore”). Third Point Offshore is handled by Third Point LLC (“Third Point” or “Investment Manager”), an SEC-registered financial investment advisor headquartered inNew York Third Point Offshore is a feeder fund to the Third Point Offshore Master Fund L.P. in a master-feeder framework. Third Point LLC, an SEC signed up financial investment advisor, is the Investment Manager to the Funds. Unless or else defined, all info consisted of here connects to the Third Point Offshore Master Fund L.P. inclusive of tradition exclusive financial investments. P&L and AUM info exist at the feeder fund degree where suitable. Sector and geographical classifications are identified by Third Point in its single discernment. Performance outcomes exist web of monitoring charges, broker agent payments, management expenditures, and accumulated efficiency allowance, if any kind of, and consist of the reinvestment of all rewards, rate of interest, and resources gains. While efficiency appropriations are accumulated monthly, they are subtracted from capitalist equilibriums just each year or upon withdrawal. From the beginning of Third Point Offshore via December 31, 2019, the fund’s historic efficiency has actually been determined utilizing the real monitoring charges and efficiency appropriations paid by the fund. The real monitoring charges and efficiency appropriations paid by the fund show a combined price of monitoring charges and efficiency appropriations based upon the heavy standard of quantities purchased various share courses based on various monitoring charge and/or efficiency allowance terms. Such monitoring charge prices have actually varied in time from 1% to 2% per year. The quantity of efficiency appropriations suitable to any kind of one capitalist in the fund will certainly differ materially depending upon many variables, consisting of without constraint: the particular terms, the day of first financial investment, the period of financial investment, the day of withdrawal, and market problems. As such, the web efficiency revealed for Third Point Offshore from beginning via December 31, 2019 is not a quote of any kind of particular capitalist’s real efficiency. For the duration start January 1, 2020, the fund’s historic efficiency reveals a measure efficiency for a brand-new problems qualified capitalist in the highest possible monitoring charge (2% per year) and efficiency allowance (20%) course of the fund, that has actually joined all side pocket exclusive financial investments (as suitable) from March 1, 2021 forward. The beginning day for Third Point Offshore Fund Ltd is December 1, 1996. All efficiency outcomes are price quotes and previous efficiency is not always a measure of future outcomes. The web P&L numbers are consisted of due to the SEC’s brand-new advertising guideline and advice. Third Point does not think that this statistics precisely shows web P&L for the referenced sub-portfolio team of financial investments as clarified a lot more totally listed below. Specifically, web P&L returns show the allowance of the highest possible monitoring charge (2% per year), along with utilize variable numerous, if suitable, and motivation allowance price (20%), and a presumed overhead proportion (0.3%), to the accumulation underlying placements in the referenced sub-portfolio team’s gross P&L. The monitoring charges and overhead are assigned through proportionately based upon the ordinary gross direct exposures of the accumulation underlying placements of the referenced sub-portfolio team. The indicated motivation allowance is based upon the reduction of the monitoring charge and expenditure proportion from Third Point Offshore fund degree gross P&L acknowledgment through. The motivation allowance is accumulated for each and every duration to just those placements within the referenced sub-portfolio team with i) favorable P&L and ii) if throughout the present MTD duration there is a reward allowance. In MTD durations where there is a turnaround of formerly accumulated motivation allowance, the influence of the turnaround will certainly be based upon the previous month’s YTD accumulated motivation allowance. The presumed running expenditure proportion kept in mind here is used consistently throughout all underlying placements in the referenced sub-portfolio team offered the fundamental problem in establishing and designating the expenditures on a sub-portfolio team basis. If expenditures were to be assigned on a below- profile team basis, the web P&L would likely be various for each and every referenced financial investment or sub-portfolio team, as suitable. While the efficiencies of the fund has actually been contrasted right here with the efficiency of widely known and commonly identified indices, the indices have actually not been picked to stand for an ideal criteria for the fund whose holdings, efficiency and volatility might vary dramatically from the protections that consist of the indices. Past efficiency is not always a measure of future outcomes. All info offered here is for educational functions just and must not be considered as a referral to get or market protections. All financial investments entail threat consisting of the loss of principal. This transmission is personal and might not be rearranged without the share written authorization of Third Point LLC and does not make up a deal to market or the solicitation of a deal to acquire any kind of safety or financial investment item. Any such deal or solicitation might just be made through distribution of an accepted personal offering memorandum. Specific business or protections received this discussion are implied to show Third Point’s financial investment design and the sorts of sectors and tools in which we spend and are not picked based upon previous efficiency. The evaluations and final thoughts of Third Point consisted of in this discussion consist of particular declarations, presumptions, price quotes and estimates that show numerous presumptions by Third Point worrying expected outcomes that are naturally based on substantial financial, affordable, and various other unpredictabilities and backups and have actually been consisted of only for illustratory functions. No depictions share or indicated, are made regarding the precision or efficiency of such declarations, presumptions, price quotes or estimates or relative to any kind of various other products here. Third Point might get, market, cover, or otherwise transform the nature, kind, or quantity of its financial investments, consisting of any kind of financial investments recognized in this letter, without additional notification and in Third Point’s single discernment and for any kind of factor. Third Point thus disclaims any kind of task to upgrade any kind of info in this letter. This letter might consist of efficiency and various other setting info associating with as soon as activist placements that are no more energetic but also for which there stay recurring holdings handled in a non-engaged way. Such holdings might remain to be classified as lobbyist throughout such holding duration for profile monitoring, threat monitoring and capitalist coverage functions, to name a few points. Information offered here, or otherwise offered relative to a possible financial investment in the Funds, might make up non-public info concerning Third Point Investors Limited, a feeder fund detailed on the London Stock Exchange, and as necessary dealing or selling the shares of the detailed tool on the basis of such info might go against protections legislations in the United Kingdom, United States and somewhere else. New Series (Excludes Legacy Private Investments) 3  1 Through September 30, 2024. Please note there is a one-month lag in efficiency showed for the CS HF Event-Driven Index 2 Annualized Return from beginning (December 1996 for TP Offshore and estimated indices). 3“New Series (Excludes Legacy Private Investments)” makes use of the existing collection performance history kind beginning via May 31, 2023. Returns from June 1, 2023 and forward omit tradition exclusive financial investments. |

Editor’s Note: The recap bullets for this write-up were picked by Seeking Alpha editors.

Editor’s Note: This write-up reviews several protections that do not trade on a significant united state exchange. Please recognize the threats connected with these supplies.